Green hydrogen companies are assets to the sustainable energy future

Due to the climate crisis, reducing reliance on fossil fuels has become one of the top priorities for many companies. One promising solution is green hydrogen, produced using renewable energy, which holds potential as a versatile fuel and energy source.

Deloitte predicts the hydrogen market's annual growth will reach approximately $1.4 trillion in revenue by 2050. Mostly, oil and gas companies and metal manufacturers are expressing huge interest in green hydrogen as their energy source due to its capacity to mitigate carbon emissions while addressing global energy requirements.

Green hydrogen (sometimes "green H2" ) is generated by using renewable sources to carry out electrolysis. The process breaks down water into its subsequent elements of hydrogen and oxygen.

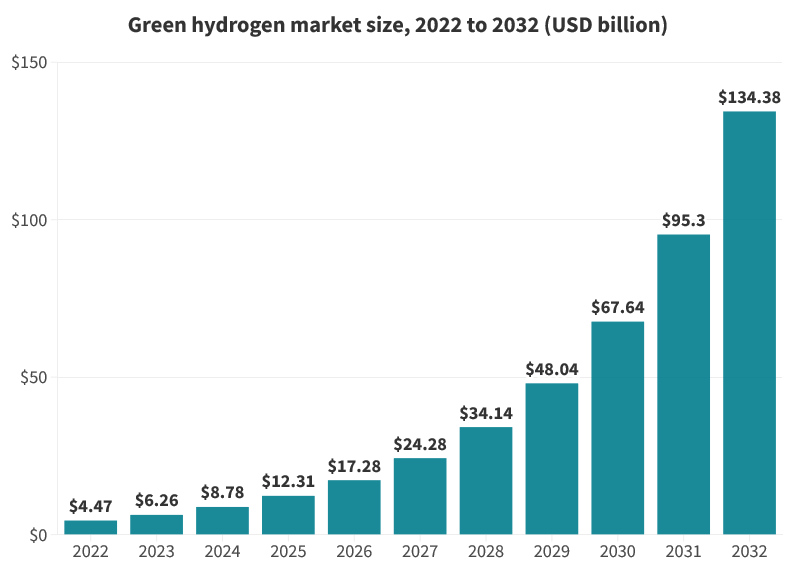

As shown in Figure 1, the green hydrogen market was valued at USD 6.26 billion in 2023 and is projected to exceed USD 134.38 billion by 2032. This shows a strong compound annual growth rate (CAGR) of 40.6%.

Although green hydrogen has a huge potential, the present scenario lacks well-established business models. But as the companies gain a deeper understanding of project risks and opportunities, we expect a shift in business models.

Related: Innovative strategies for businesses to attain Net Zero ready status

Green and clean hydrogen companies

Several crucial factors will play a decisive role in the hydrogen industry. This includes access to renewables, engagement, innovation pace, and transportation for storage. The current major problem is that the companies seek a one-size-fits-all solution, which is not feasible in many cases.

In reality, the capabilities of the hydrogen supply chain and overall project development become key factors in determining the right solution. Furthermore, the availability of resources in these areas and the potential for forming partnerships with different stakeholders in the production chain are crucial considerations.

Green hydrogen companies are on the brink of experiencing significant growth due to a remarkable increase in supply and demand for environmentally friendly hydrogen. The installation of electrolyzers is projected to reach 242 GW within 2030 with a cumulative investment of approximately $130 billion.

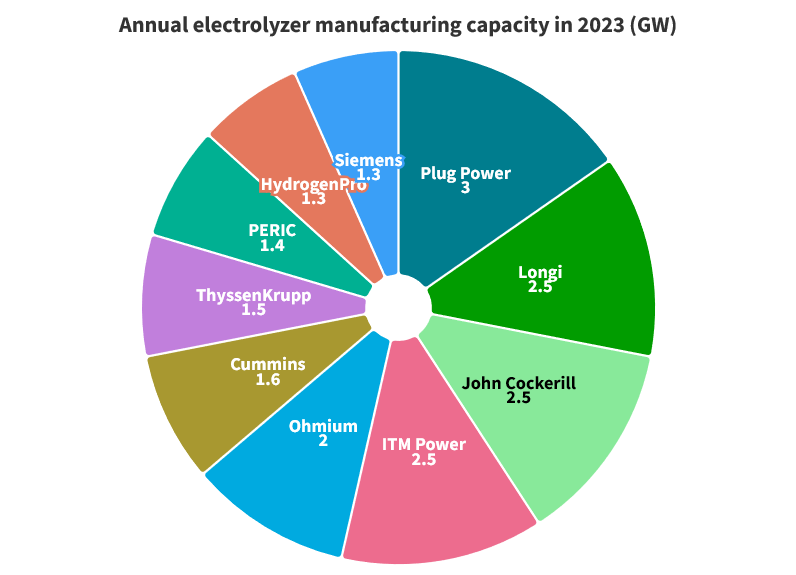

Leading manufacturers in 2023 include Longi Green Technology, John Cockerill, Plug Power, ITM Power, and many more (Figure 2). However, the definition of clean hydrogen is slightly different than green hydrogen. While green hydrogen is solely dependent on sustainable sources like solar or wind power, clean hydrogen includes the production using both renewables and fossil fuels, employing carbon capture and storage (CCS) technology.

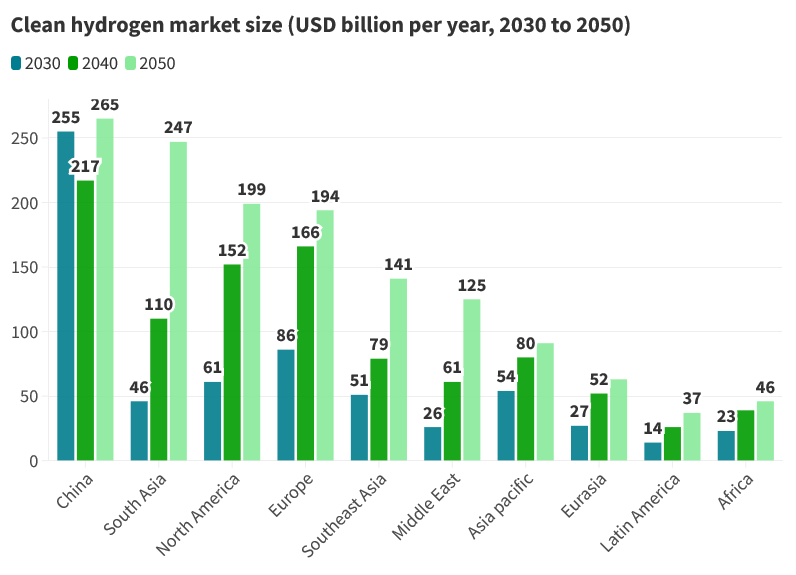

The clean hydrogen market size looks equally appealing. In 2022, the Asia-Pacific region emerged as the dominant force in the global hydrogen market. Especially, China stands as the global leader, contributing to one-third of the total global production (Figure 3). The North American clean hydrogen market is expected to be valued at USD 61 billion in 2030.

Challenges

In a net-zero emissions world, green hydrogen offers a solution for challenging-to-decarbonize sectors like steel, manufacturing, and heavy-duty transport. However, despite the prospects for high growth, there are potential challenges in the upcoming phase:

- Green hydrogen companies face high production costs, primarily driven by the electrolyzers used to split water molecules. The technology behind electrolyzers is still in a relatively early stage of development, resulting in expensive equipment.

- Infrastructure limitations are another challenge due to its low energy density, making efficient transportation and storage a complex task. The limited availability of hydrogen pipelines and large-scale transportation can be costly and complicated.

- In underdeveloped areas, there is often a lack of awareness accompanied by economic challenges and limited infrastructure. This deficiency in infrastructure poses challenges for the effective establishment and distribution of green hydrogen projects.

- The upfront investment cost required for establishing hydrogen infrastructure and the associated high maintenance costs stands out as another challenge hampering the market growth.

- Green hydrogen needs a significant portion of electricity from renewable sources for the process to take place. This may be not feasible in many areas.

Related: Heavy industry: how to operate sustainably in the modern era?

Growing opportunity for the companies

Currently, fossil fuels contribute to 96% of the hydrogen production. Renewable sources, especially, wind farms have shown great potential in replacing fossil fuels. The cost of wind energy has reduced over the past few decades, making it an eligible source of green hydrogen production.

Related: Renewable energy investments call for stronger commitment to net-zero initiatives

By increasing investments in research and development, scientists and engineers can identify optimization methods to enhance efficiency and reduce reliance on expensive materials. This will result in lower production costs, attract investments, and foster increased market adoption.

In particular, renewable energy production, and decarbonization processes can open growth opportunities in hydrogen storage and transportation techniques, along with the establishment of hydrogen refueling stations. As the infrastructure continues to advance, it fosters increased opportunities for the widespread adoption of green hydrogen.

Related: Strategies for businesses to overcome sustainability challenges and thrive

Green hydrogen has a greener future

In 2030, Asia is expected to dominate the market, capturing 55%, driven by increasing demand in China, India, and Indonesia.

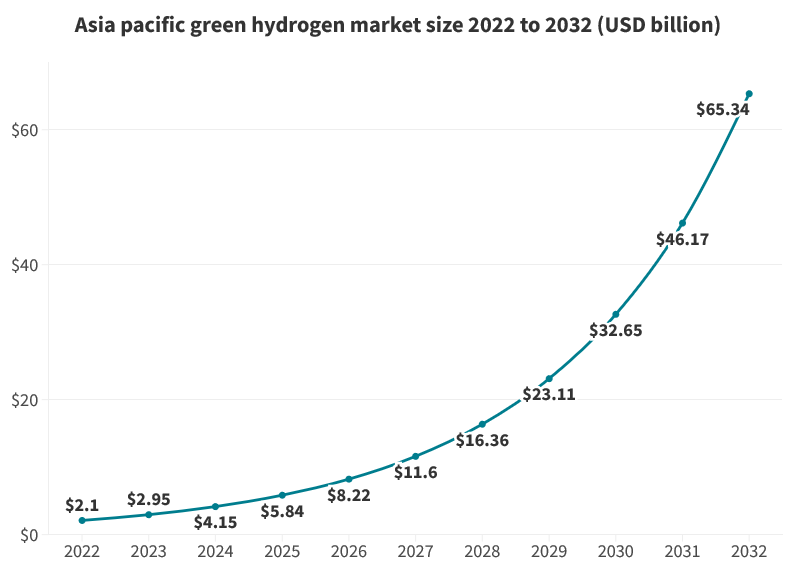

The Asia-Pacific green hydrogen market attained a size of USD 2.95 billion in 2023 and is projected to achieve approximately USD 65.34 billion by 2032, reflecting a notable CAGR of 41.1% from 2023 to 2032 (Figure 4).

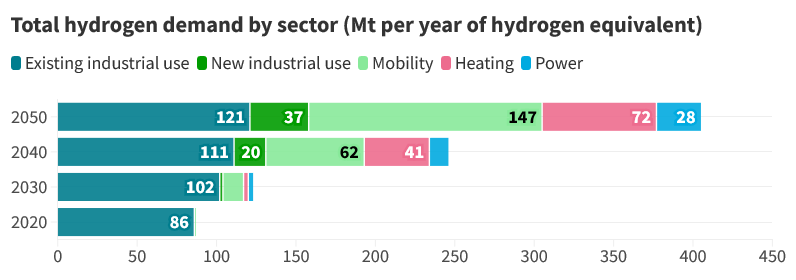

By the year 2050, hydrogen is anticipated to assume a more prominent role in various applications, particularly in the field of mobility. According to McKinsey, mobility could be the primary new sector driving demand for hydrogen by 2050. This surge in demand may span from fuel-cell electric vehicles for long-haul, heavy-duty trucking to the use of synthetic kerosene in aviation.

When considering both the adoption in existing applications and its emergence in new sectors, clean hydrogen's share of total demand could reach 95% by the year 2050 (Figure 5).

Until then, there still needs to be done. The implementation of regulations favoring green hydrogen within the energy sector will substantially boost the market's revenue. Additionally, the ability to conveniently store green hydrogen for later use will be another factor driving market growth.