Climate-linked disasters costing billions: insurers urged to act to avoid catastrophe

In recent weeks, thousands of people in California remained under evacuation due to flooding that left at least 20 dead. Only 230,000 properties in California, i.e. about 2% are believed to have flood insurance policies.

In Europe, flooding is unusual in winter but this year, it was no exception. Heavy rains have caused flooding on several waterways in northern Hungary this month. In the north, Channel Island, Jersey also experienced a flood, causing about 50 families to leave their homes.

In recent years, climate change has escalated the frequency and intensity of extreme flood events. Last summer, Pakistan’s devastating flood impacted around 33 million people, killing more than 1,000. By mid-January 2023, as many as 4 million children were still living near contaminated flood waters.

Going back a little further to reminisce other natural calamities— not long ago in 2017, Hurricane Harvey caused USD ($)125 billion in economic damage. In another part of the world, the Australian bushfires damaged at least 3,500 homes and thousands of other buildings, damaging more than $4.4 billion in 2019-2020. More frequently than the record can handle, natural disasters are destroying homes, destructing the whole ecosystem, and indirectly affecting the least anticipated industry: Insurance.

Climate Change means insurance risk

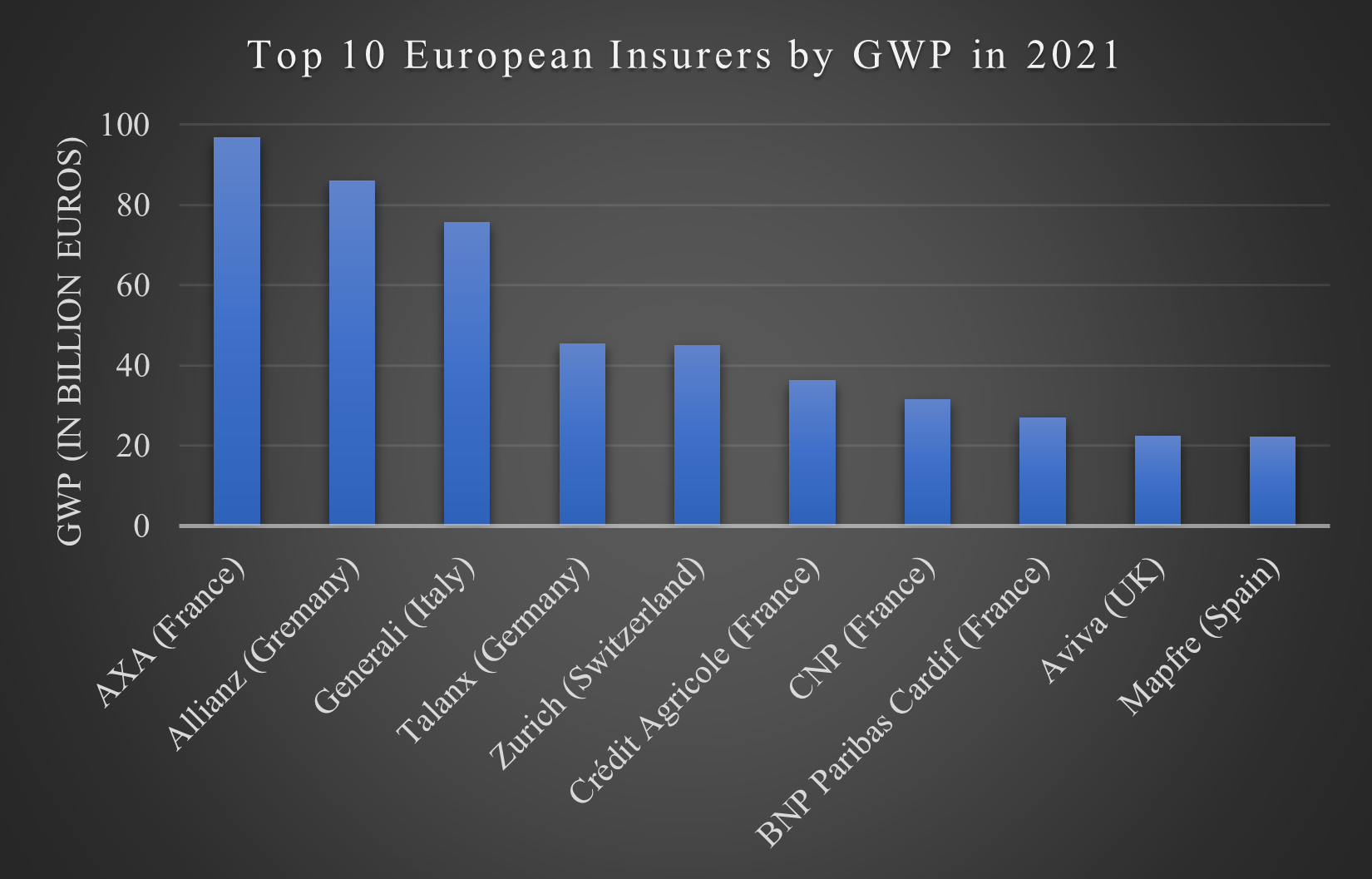

As the magnitude of climate change is observed more frequently, insurers have started noticing the sudden threat to their business models. The unprecedented catastrophic events have threatened companies and if not done something urgently, this only means a lose-lose situation for everyone— unaffordable for customers and unfeasible for insurers. Figure 1 demonstrates the top 10 European insurers by gross written premium (GWP) in 2021.

According to a 2020 Triple-I Consumer poll, only 27% of homeowners in the US have flood insurance, which is separate from home insurance. The owners, who have home insurance (i.e. 85% of the US population) are paying an average of $1,445 per year. This is a huge sum for the majority of citizens and the insurance will cost even more as the risk of climate change increases. Despite the knowledge of the insurance market, too many people are obliged to remain uninsured for the impact caused by these events.

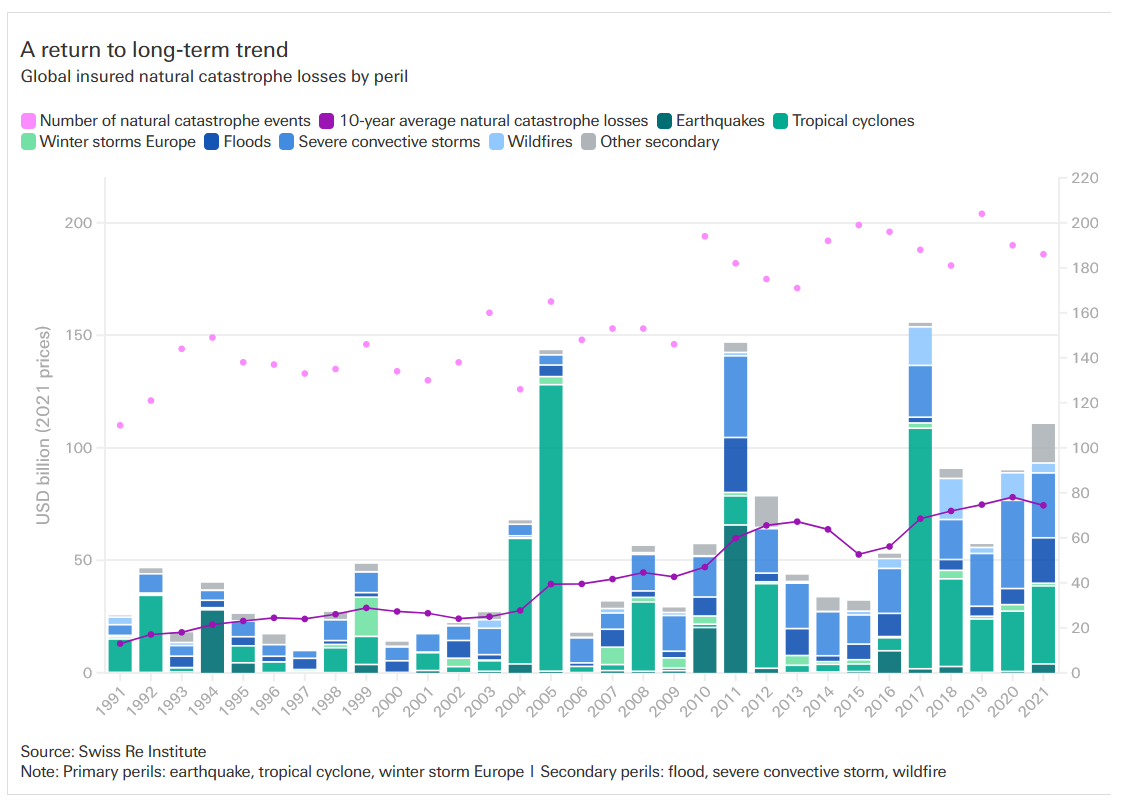

Figure 2 summarizes the global insured natural catastrophe losses by peril— a study done by the Swiss Re Institute. According to the study, global insured losses from floods were $80 billion from 2011 to 2020. Only 18% of global economic losses were insured. In 2021, the world saw more than 50 severe flood events with estimated combined economic losses of more than $80 billion. Beyond flood events, the year 2021 saw economic losses of $270 billion and insured losses of $111 billion from natural catastrophes.

How to minimize the damage?

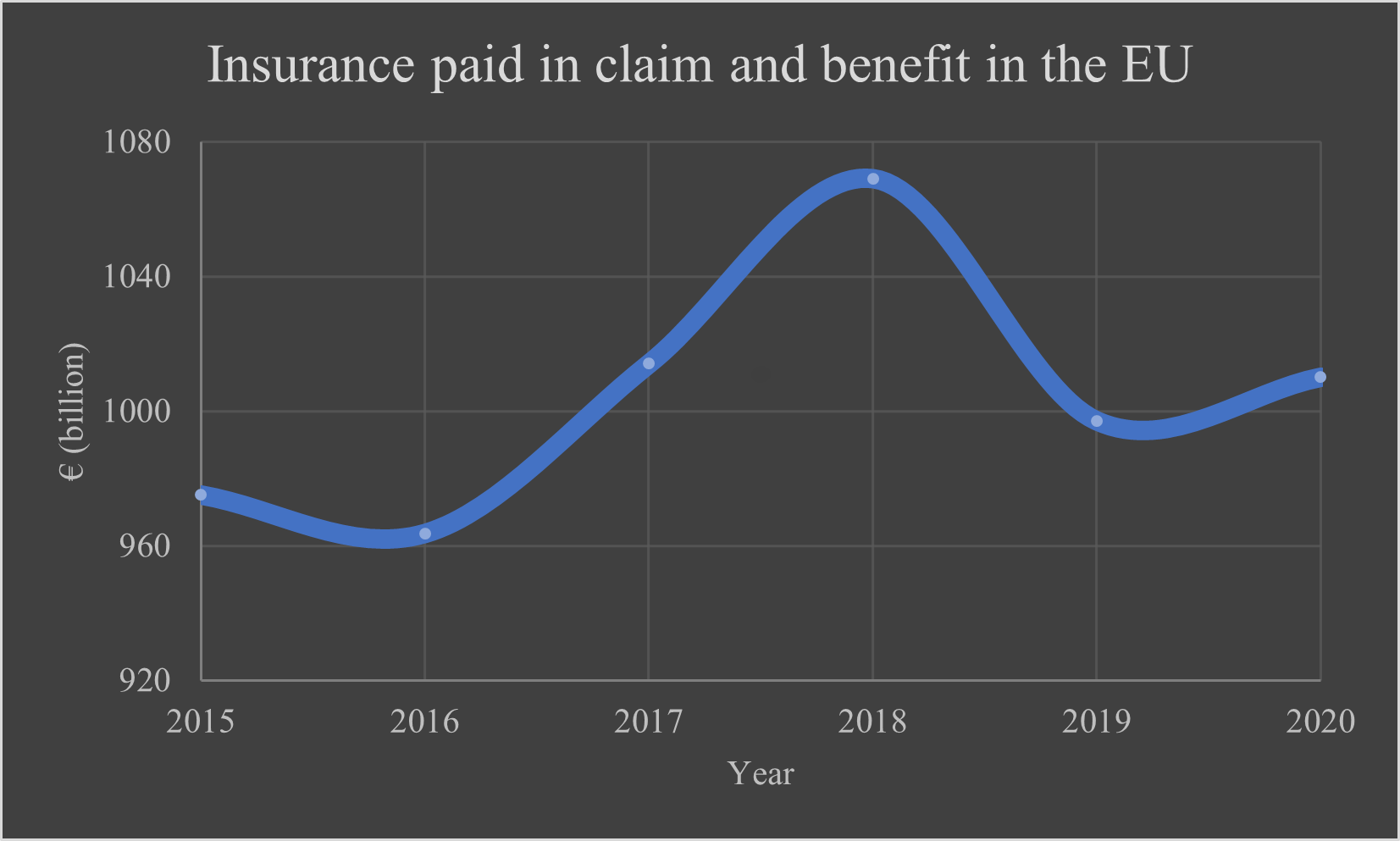

In Europe, heat stress is a growing concern. The region endured two recording-breaking heat waves within two months during the summer of 2019. The continent also experienced the warmest on record from 2009-2018, with temperatures around 1.7°C above the pre-industrial era. Long stretches of summer heat and thunderstorms cause a sudden change in weather, inducing flash floods. Figure 3 summarizes the amount of insurance paid in claims and benefit in the EU from 2015 until 2020.

Read: Deadly heat wave shrinks work efficiency

Read: Heat wave grips Europe: Climate crisis intensifies

Read: European Glaciers Are Disappearing

The European Environment Agency (EEA) said adding insurance content to climate change could be one of the crucial steps to increase societies' capability to recover from disasters. However, one can only minimize the damage by understanding the risk in the first place.

Insurers are expected to do more to prevent worsening climate-related losses and mitigate the impact of such risks. The US state regulators and lawmakers are watching the implications of climate-related risks very carefully and are becoming increasingly concerned about the insurance industry’s response to climate change.

A survey conducted by the Deloitte Center for Financial Services found a majority of US state insurance regulators expect all types of insurance companies’ climate change risks to increase over the medium to long term—including physical risks, liability risks, and transition risks.

Insurers’ social responsibilities

The EEA report estimates that the climate crisis will destroy 167 million homes in the next 20 years. Between 1980 to 2020, deaths caused by weather extremes were between 85,000 and 145,000, which contributed to economic losses between €450-€520 billion ($514-$594 billion) over the 40 years. Germany bore the highest economic losses of €110 billion, followed by France and Italy.

However, the true damaging scale of climate change is hard to measure. Insurance companies face the dual challenge of addressing escalating climate change risks and shifting industry regulations to explore action items to achieve greater resilience.

In the climate change discussion led by McKinsey senior partner Kurt Strovink with senior partners Kia Javanmardian (P&C) and Dickon Pinner (McKinsey) and Antonio Grimaldi (McKinsey), they touched upon the importance of insurers working with customers on adapting to climate change, which means increasing resilience of their infrastructures. Here are five identified opportunities for insurers to become more resilient to climate-related risks:

- Having a net-zero target within the organization will help the organizations review its energy use and the eco-effectiveness of its operations. The UN Environmental Programme established the Net-Zero Insurance Alliance( NZIA), a group of over 29 of the world’s leading insurers to support their commitment to moving their underwriting portfolios to net-zero by 2050. They launched the first Target-Setting Protocol at the 2023 World Economic Forum’s Annual Meeting in Davos. Many insurers have committed to reducing their exposure to carbon- extreme diligence. One good example is State Farm, which announced in 2021 its internal strategy for reducing greenhouse gas emissions by 50% by 2030. They also increased paperless billing among guests while working towards removing single-use plastic water bottles from services around the country. To have an ambitious net-zero target, the companies require a clear governance structure, including clear dedicated roles for all employees.

- With the complexity of a changing climate, assessing climate threats needs advanced analytics to eliminate any uncertainty caused by loss and fluctuating data. Advanced analytics could help insurers assess literal rainfall records, property data, and hypothetical unborn climate conditions to observe threats in advance. Insurance companies can use their sophisticated understanding and resources of ongoing risks to reprice and rearrange portfolios to avoid long-term exposure to climate events. They need a wide range of plausible climate-change scenarios to determine the climate data that can be used in risk modeling for pricing and underwriting decisions.

- Maintaining accountability and transparency is crucial for both internal employees and external stakeholders. As the climate is changing drastically and in high frequency, any previously estimated threat exposure could become questionable at one point. Accenture’s research shows about 72% of executives keep sustainability as their top priority. Ignoring accountability and transparency around sustainability means insurers are missing an opportunity to attract new customers and their loyalty.

- Private-public partnerships and collaboration could work between the insurers and policymakers to produce a sustainable model rather than making premiums unaffordable, which can increase the uninsured number. Individual insurers can also work to educate policyholders about severe rainfall events and work proactively with agencies to develop climate-flexible public programs in high-threat zones. Similarly, building design and retrofitting homes could be incentivized through government programs to make them more resilient to natural catastrophes.

- Offering innovative products that address climate concerns will reshape the way we approach sustainability in the enterprise and beyond. Climate change will bring new hazards at an unimaginable stage that requires new products and new underwriting solutions. In the next five years, the Environment, Social, and Governance (ESG) trends are projected to drive a $206 billion opportunity— which means great opportunities for the insurers that include climate risk assessment more consistently in their business framework. Insurers should re-address their investment strategies and feel responsible to bring industries to a less severe risk. Swiss Re recently teamed up with The Nature Conservancy and regional governments in Mexico to develop a cutting-edge product that protects the coral reef off the coast of the Yucatan Peninsula—essentially, underwriting nature.

Insurers should go beyond traditional assessment of threat transfer to explicitly address them with mitigation. With more and more extreme weather events around the world, they have an opportunity to showcase the efficacy of actions they may be taking to assess and mitigate climate-related risks. Insurance leaders who do this will stand out in the market.

Summary

- Climate change has escalated the frequency and intensity of extreme natural disasters in recent years

- In recent weeks, thousands of Californians remained under evacuation orders as the flooding left at least 20 dead

- According to Swiss Re, global insured losses from floods from 2011 to 2020 were $80 billion

- In the same timeframe, about 82% of global economic losses from floods were uninsured

- Insurers are expected to do more to prevent worsening climate-related losses